Update on Economic Indicators

As of the end of October and early November 2025, the housing market and broader economic indicators across San Mateo County and the Bay Area reflect a mix of moderating inflation, shifting mortgage rates, and continued-but uneven-market activity. Equity markets reached new highs earlier in the fall, 30-year mortgage rates dropped to their lowest levels in more than a year, and the Federal Reserve implemented two quarter-point rate cuts in 2025. Despite these improvements, general consumer confidence remains subdued, with many households still experiencing concerns about job security, inflation, and overall financial stability. Affluent buyers, buoyed by strong stock market gains, appear less concerned.

The Economic Policy Uncertainty Index has continued to ease from its tariff-shock peak earlier in the year but still sits above long-term historical averages.

Home Price Trends

Single-Family Homes

-

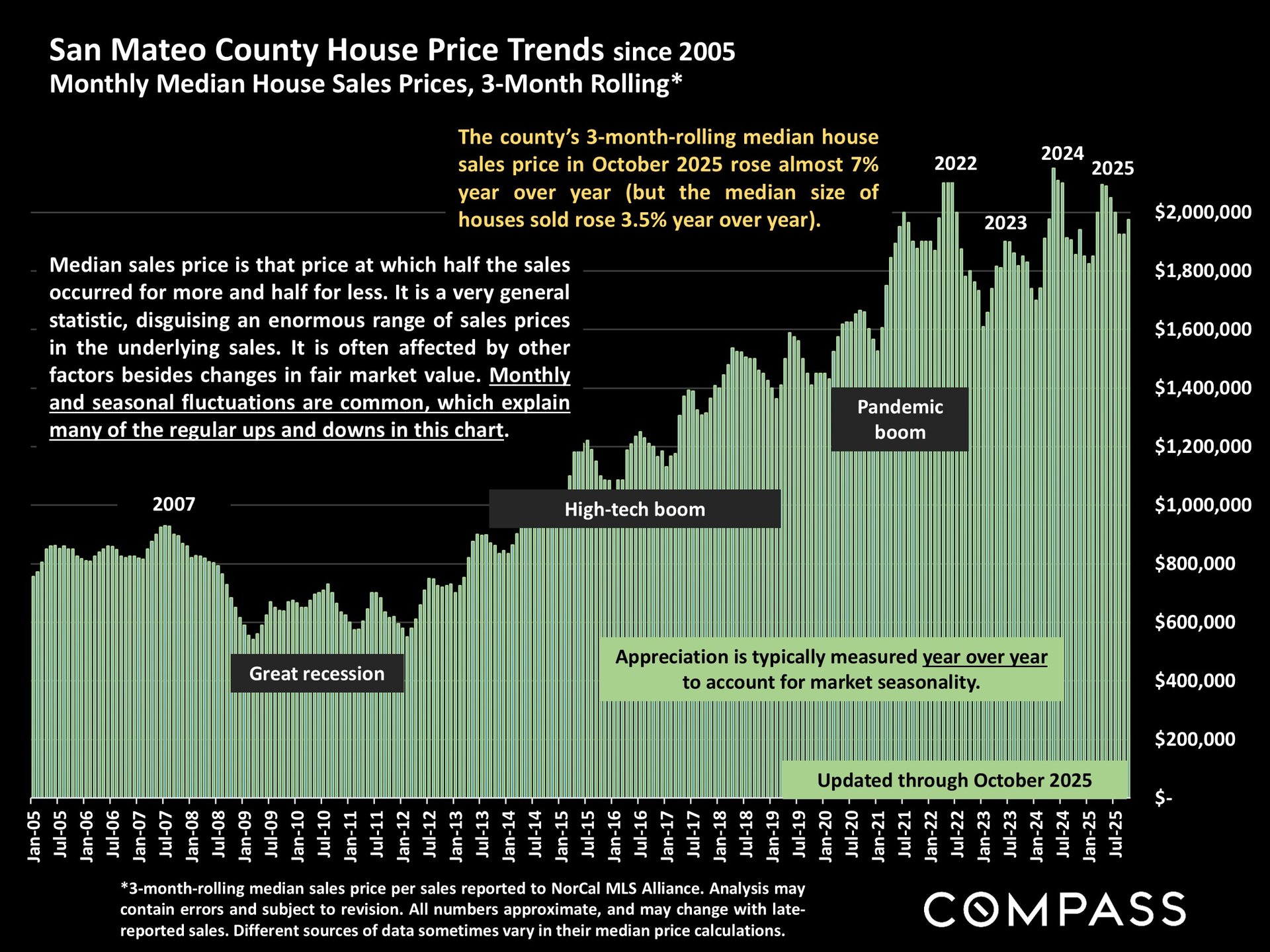

The 3-month rolling median house price in San Mateo County rose almost 7% year over year as of October 2025.

-

Median house size also increased 3.5% YoY, affecting median price trends.

-

Home prices remain near the elevated levels reached during 2022 and 2024 peak periods.

-

Monthly and seasonal fluctuations continue to create predictable ups and downs throughout the year, but long-term appreciation remains strong compared to pre-pandemic norms.

Condos

-

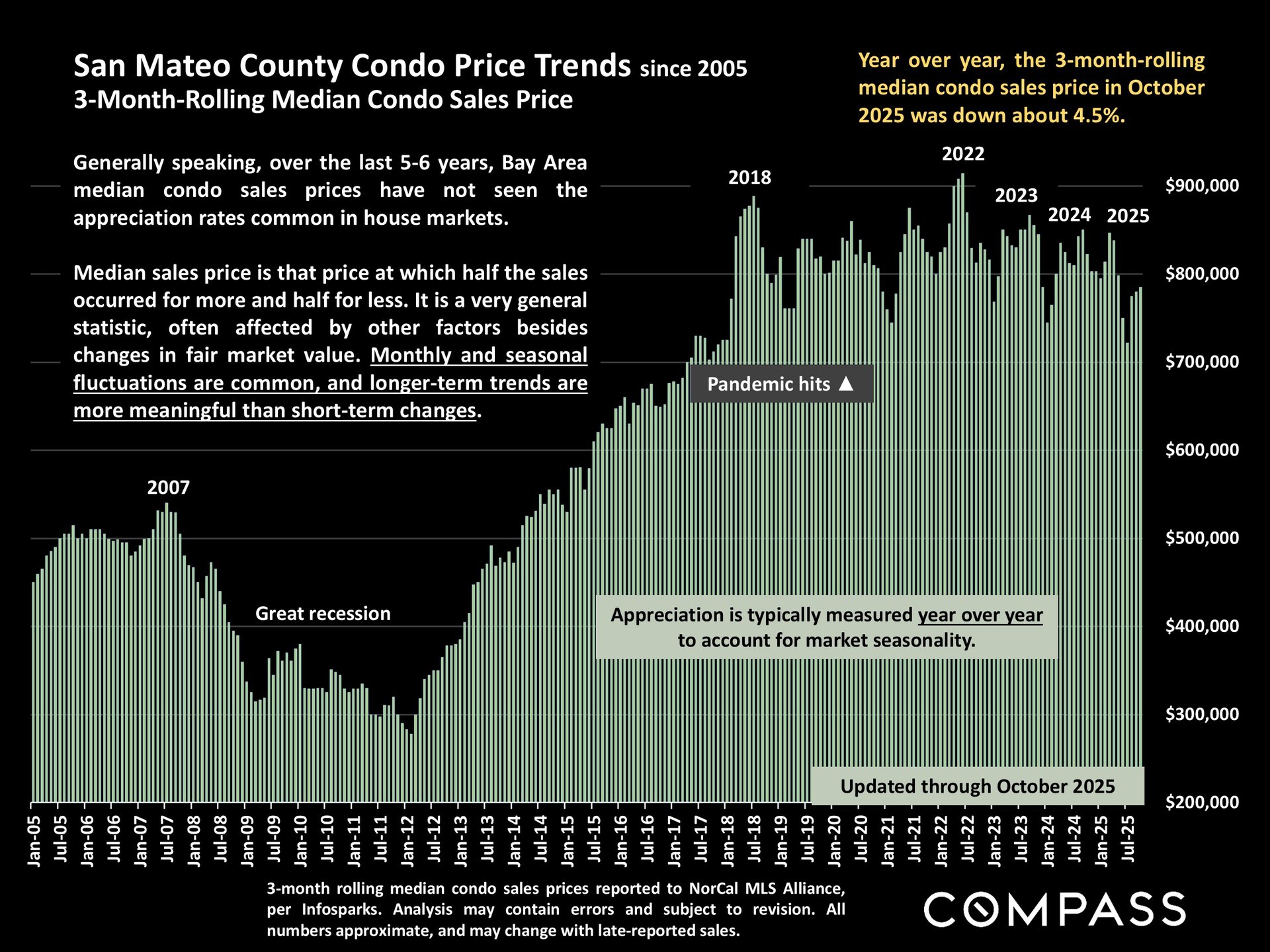

The 3-month rolling median condo price in October 2025 was down ~4.5% YoY.

-

Over the past 5–6 years, Bay Area condos have not matched the appreciation seen in single-family homes.

-

Seasonal and monthly volatility remain pronounced, and longer-term trends are generally more meaningful than short-term shifts.

-

Dollar per Square Foot

-

Median $/sq.ft. values for houses remain significantly above pre-pandemic levels, with 2025 readings trailing slightly below the 2022 peak.

-

Condo $/sq.ft. values display similar fluctuation patterns but at lower overall levels.

-

Seasonal variations remain a major driver of the oscillations visible in the data, while the pandemic period reflects a sharp and sustained increase across property types.

-

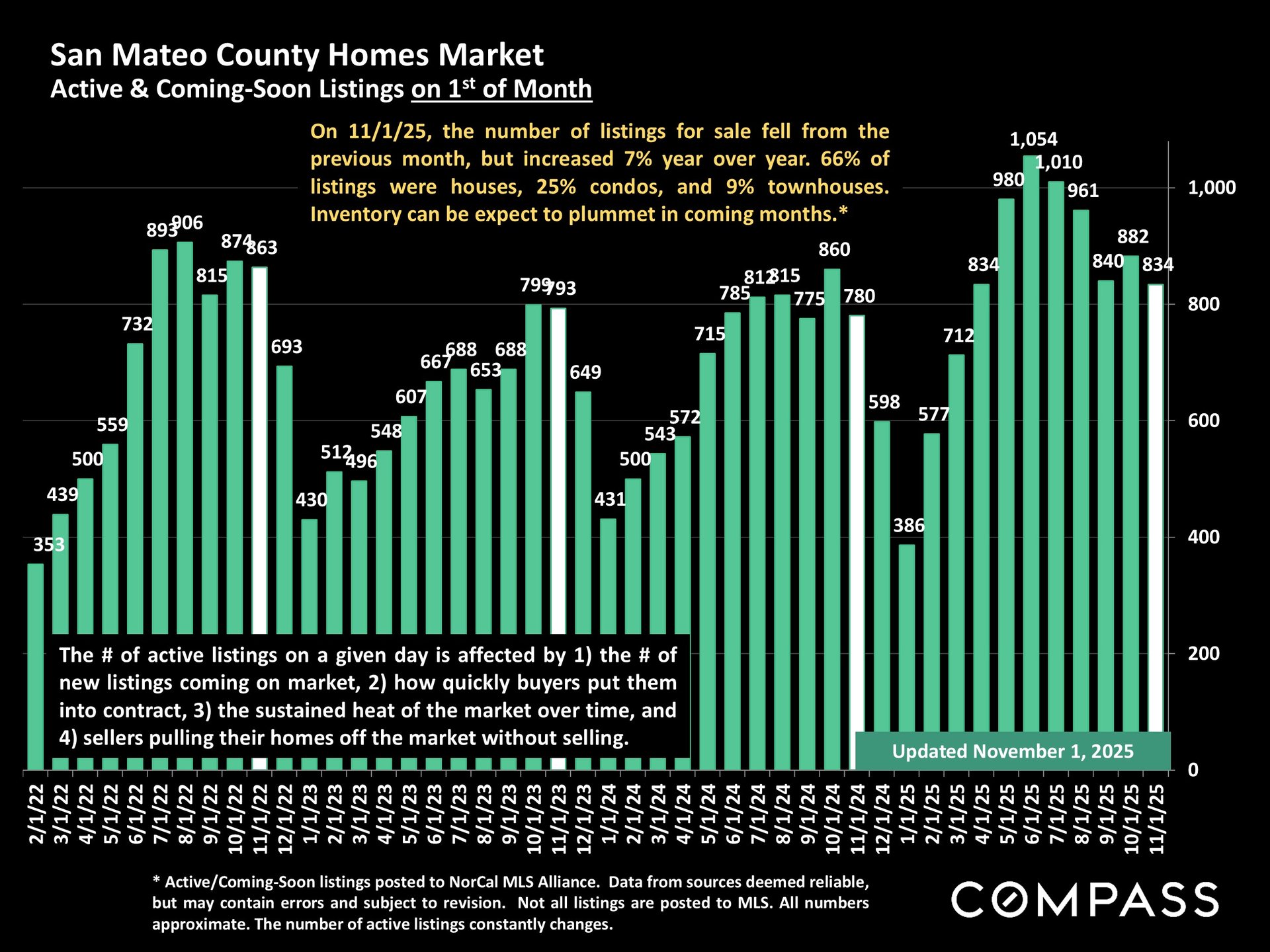

Inventory & Listings

As of November 1, 2025:

-

Active and coming-soon listings fell month over month but were up 7% year over year.

-

Inventory composition:

-

66% houses

-

25% condos

-

9% townhomes

-

-

Inventory levels tend to drop sharply heading into the late-fall and early-winter months, and 2025 appears aligned with that seasonal trend.

The number of active listings on any given date is affected by:

-

The flow of new homes coming to market

-

The speed at which buyers put homes into contract

-

The strength and “heat” of the broader market

-

Sellers removing listings without selling

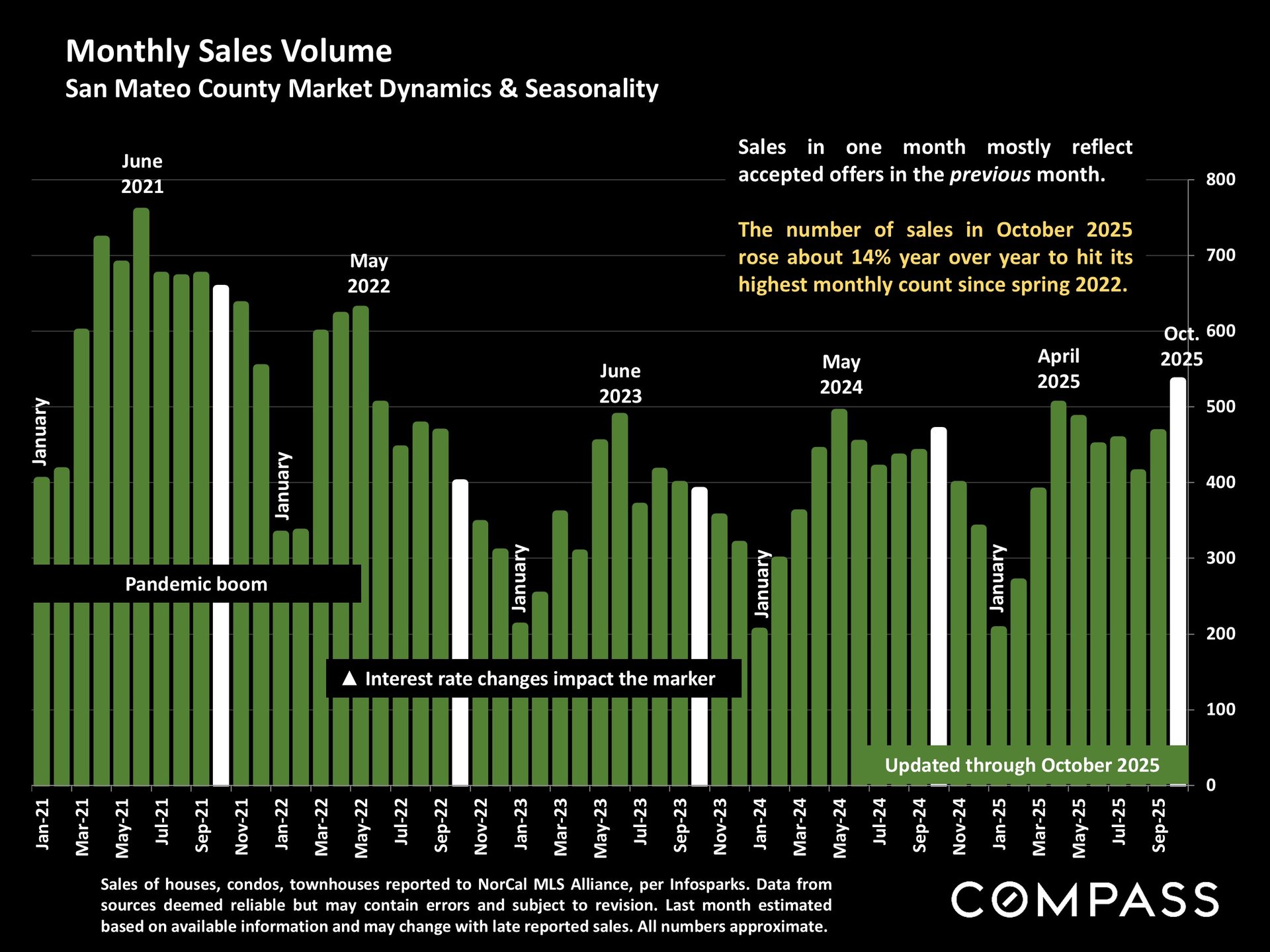

Sales Volume & Market Activity

-

October 2025 sales volume rose ~14% year over year, reaching the highest monthly count since spring 2022.

-

Sales counts in a given month typically reflect offers accepted in the previous month.

-

Seasonal slowdowns are common from mid-November through mid-January, though listings and closings still occur year-round.

-

Historically, this seasonal window provides the strongest negotiating leverage for buyers targeting homes listed earlier in the year.

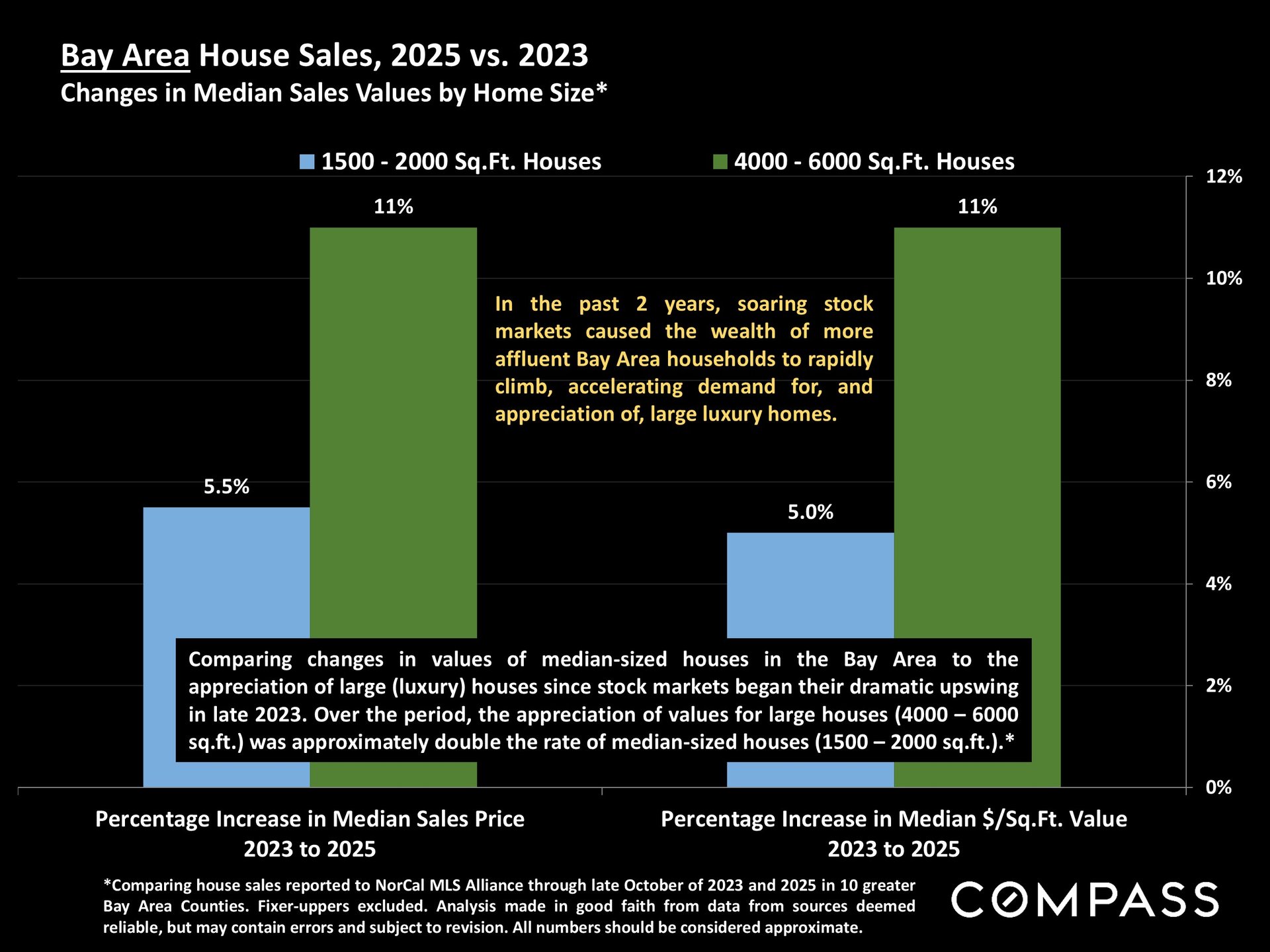

Market Segmentation by Home Size (Bay Area, 2023–2025)

Comparing median values between 2023 and 2025:

1500–2000 sq.ft. Homes

-

Median sales price up 5.5%

-

Median $/sq.ft. value up 5.0%

4000–6000 sq.ft. Luxury Homes

-

Median sales price up 11%

-

Median $/sq.ft. value up 11%

Affluent households experienced significant wealth increases during the stock market surge of late 2023 onward, sharply increasing demand for large luxury properties and driving much more rapid appreciation in that segment compared to mid-sized homes.

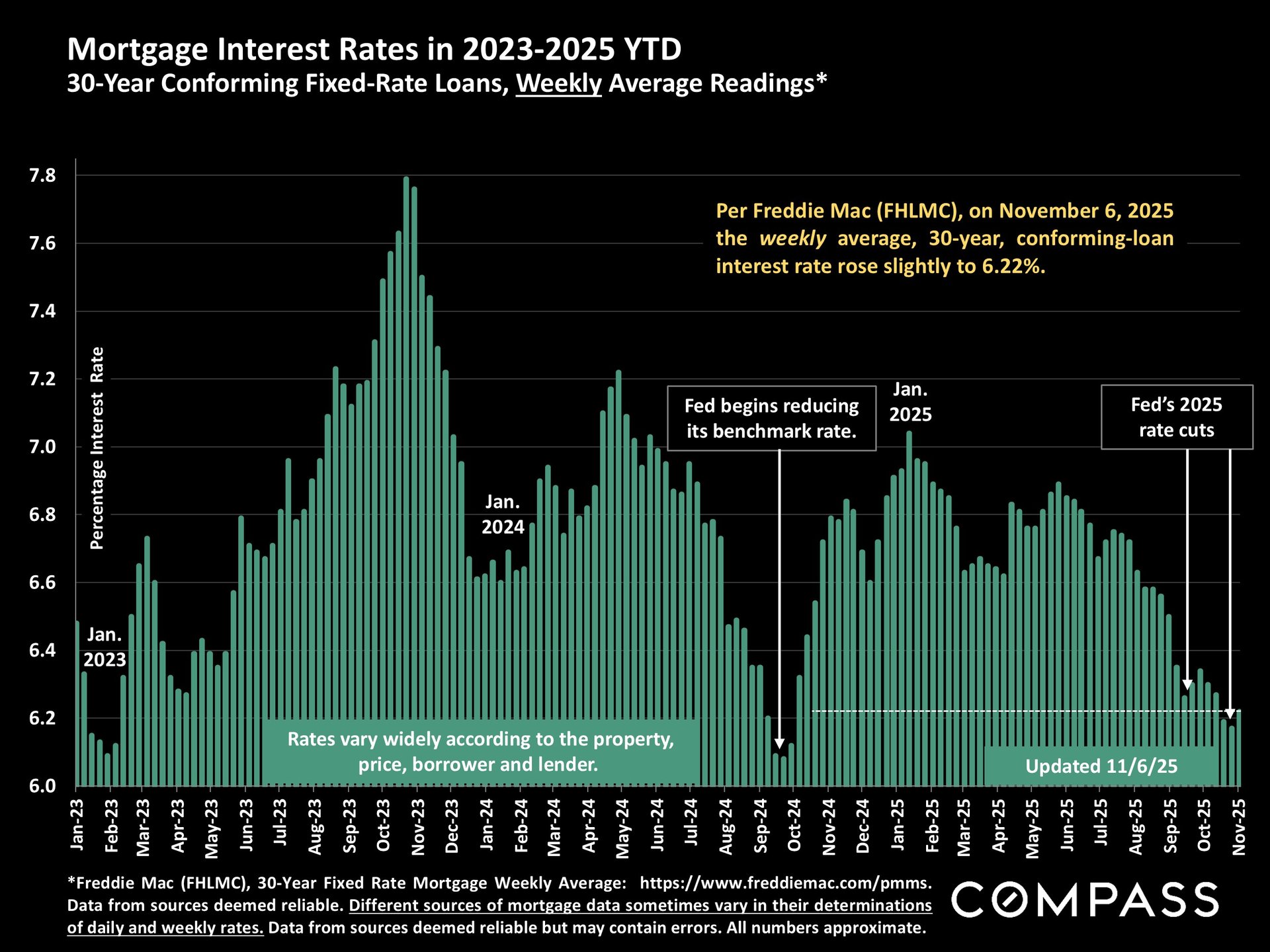

Mortgage Rates (Weekly Avg, 2023–2025)

-

Mortgage rates peaked in 2023 and early 2024 before gradually declining.

-

As of early November 2025, the weekly average 30-year fixed rate is 6.22%.

-

Notable milestones:

-

Jan 2023: ~6.2%

-

Peak near late 2023: ~7.8%

-

Jan 2024 & Jan 2025: seasonal rate spikes

-

2025 Fed rate cuts provided modest downward momentum

-

-

Rate trends vary widely based on borrower profile, property type, and lender.

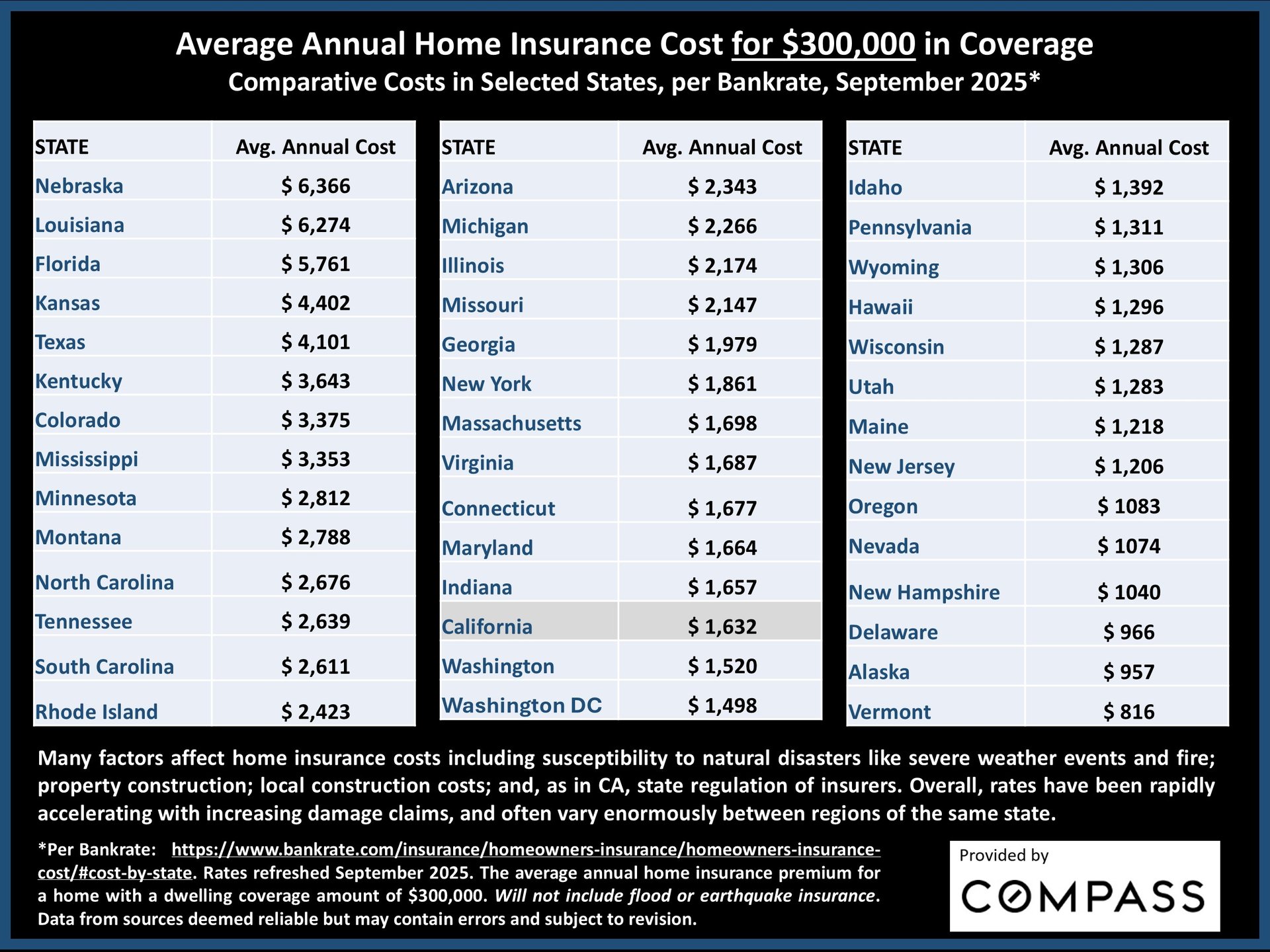

Home Insurance Costs (2025 Comparative Data)

Average annual premiums for $300,000 in dwelling coverage vary significantly by state:

-

Highest-cost states include:

-

Nebraska ($6,366)

-

Louisiana ($6,274)

-

Florida ($5,761)

-

-

Moderate-cost states include:

-

California ($1,632)

-

Arizona ($2,343)

-

New York ($1,861)

-

-

Lowest-cost states include:

-

Vermont ($816)

-

Alaska ($957)

-

Delaware ($966)

-

Rates depend on factors such as natural disaster exposure, local construction costs, and state insurance regulation.

Overall Market Takeaways

-

Home prices (single-family) remain strong, with solid YoY appreciation into late 2025.

-

Condo values remain more volatile and show YoY softening.

-

Sales volume is rising, reaching multi-year highs as of October 2025.

-

Inventory is up year over year but declining seasonally heading into winter.

-

Mortgage rates have eased from peak levels but remain elevated relative to pre-2022 norms.

-

Luxury homes significantly outperform mid-sized homes in appreciation due to wealth gains among affluent buyers.

-

Insurance costs vary dramatically nationwide, with California in the mid-range.