2025 Profile of Home Buyers and Sellers

The Housing Market Is Shifting Dramatically Older

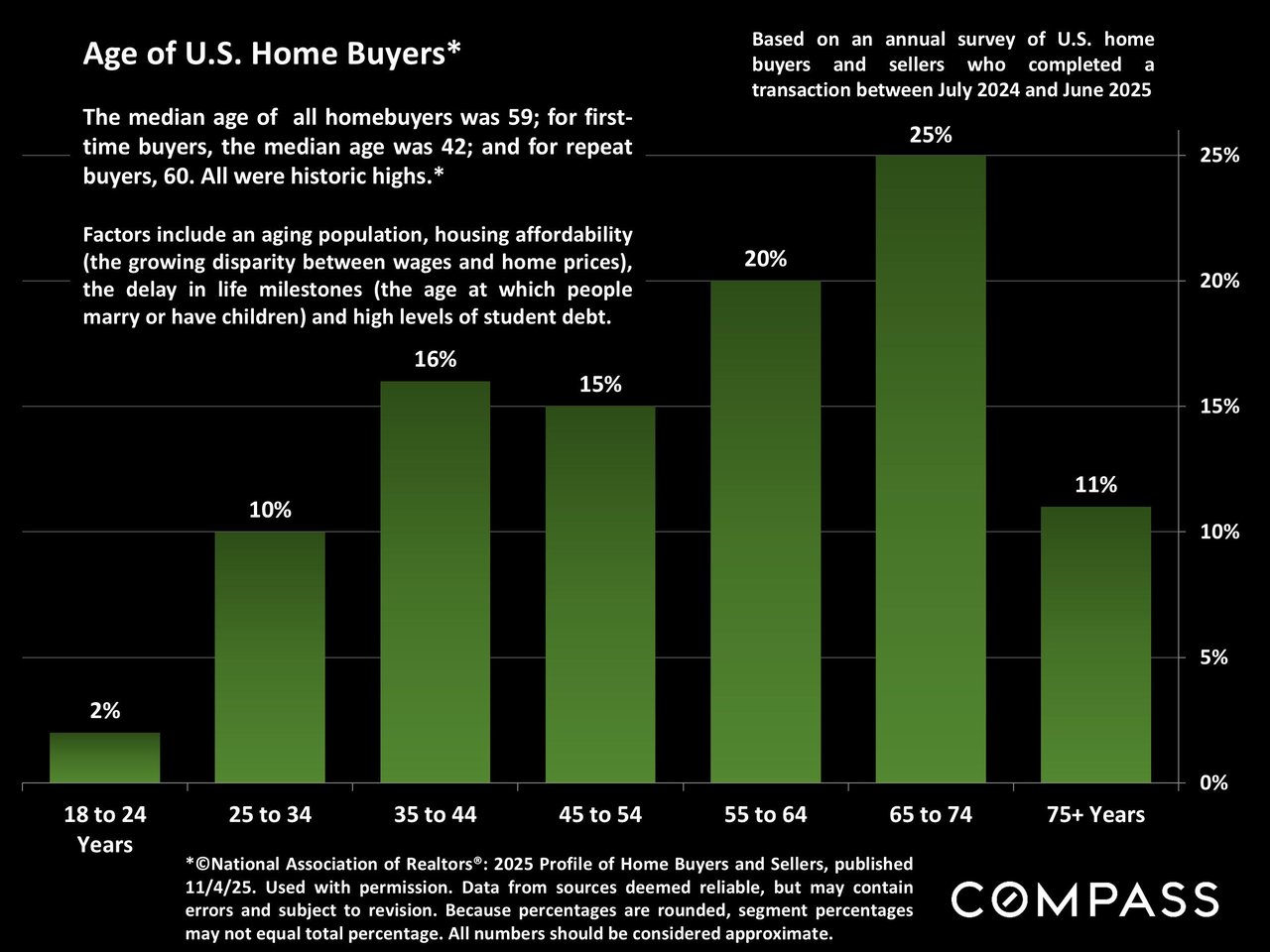

New data from the National Association of Realtors® shows a historically unprecedented shift in the age of U.S. homebuyers:

-

Median age of all buyers: 59

-

Median first-time buyer: 42

-

Median repeat buyer: 60

These are the highest readings ever recorded.

The distribution shows how skewed the market has become:

-

65–74 years: 25%

-

55–64 years: 20%

-

35–44 years: 16%

-

45–54 years: 15%

-

Very few buyers under 34

Factors driving the aging of the buyer pool include:

-

Housing affordability challenges

-

Delayed life milestones

-

High student debt

-

Wage-price divergence

-

An aging population

Younger buyers-especially those who would traditionally be first-time entrants-are being pushed out by financial barriers and debt loads.

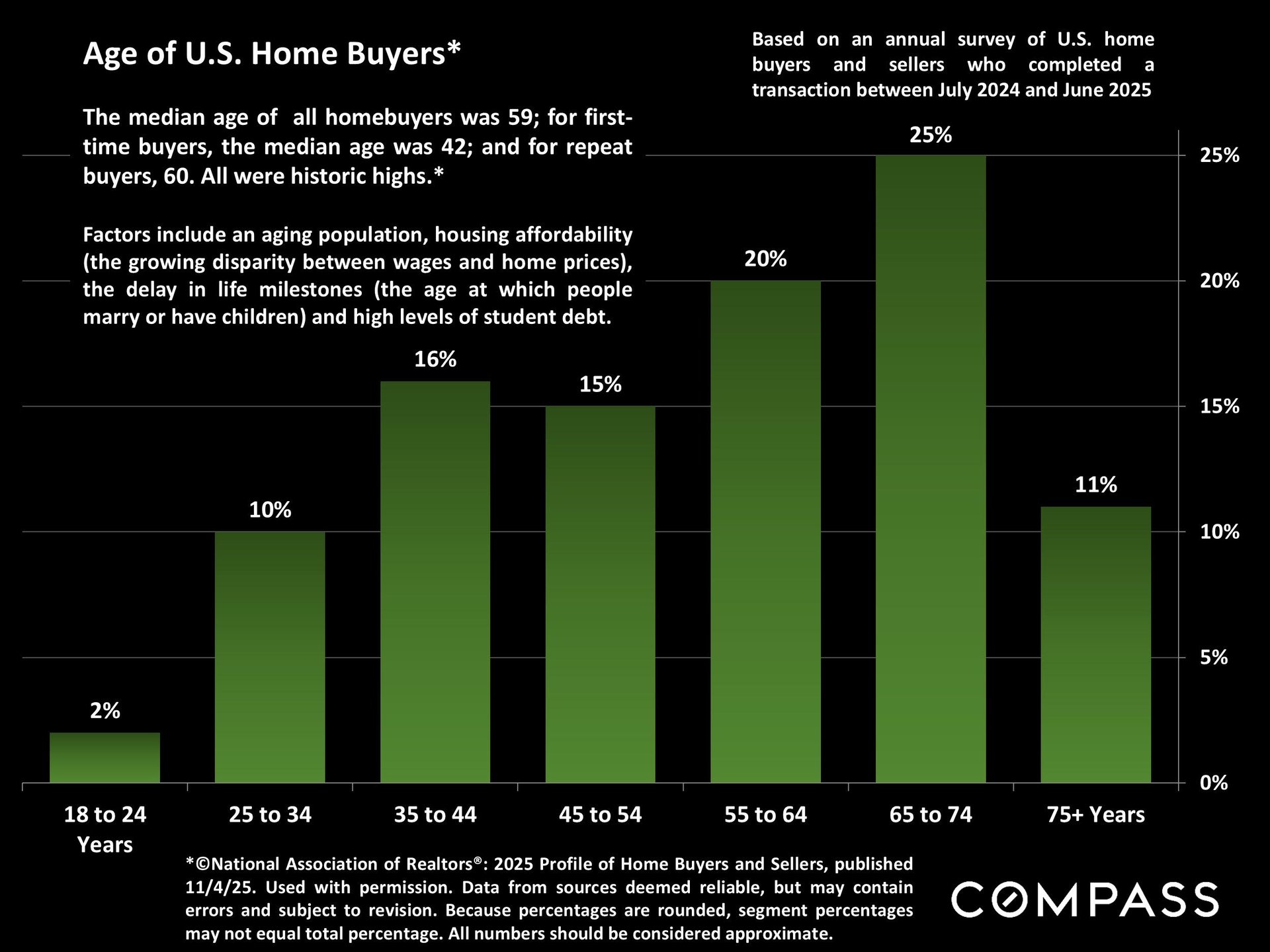

Mortgage Rates

Mortgage interest rates remained essentially unchanged from the previous week, and are still running significantly lower than during most of 2025.

However, despite the easing, buyers remain rate-sensitive and highly selective.

Stock Markets: High but Unsettled

Stock markets have been rocky recently, yet still sit at very elevated levels.

One of the primary valuation tools, the Price/Earnings (PE) Ratio, is now:

-

Well above its long-term average

-

At its highest level since the pandemic boom

The Economist (11/8/25) reported that the S&P 500 is trading at 40× underlying, cyclically adjusted earnings-a level exceeded only during the dot-com bubble, and only slightly then. Their article was pointedly titled “Before the Fall.”

No forecast is made here; rather, this indicates heightened sensitivity in markets that heavily influence affluent homebuyer behavior.

Job Market Shifts & Impacts on Housing Demand

From John Burns Research (11/12/25):

-

High-income job losses are reshaping demand

-

Sectors shrinking across most major metros include:

-

Information

-

Professional Services

-

Financial Activities

-

These sectors historically drive for-sale housing demand more than rentals.

Nationally, high-income sector employment remained flat YOY in August, well below its long-term growth trend of +1.6%.

Uncertainty remains around whether this shift will have a mild or significant impact on housing.

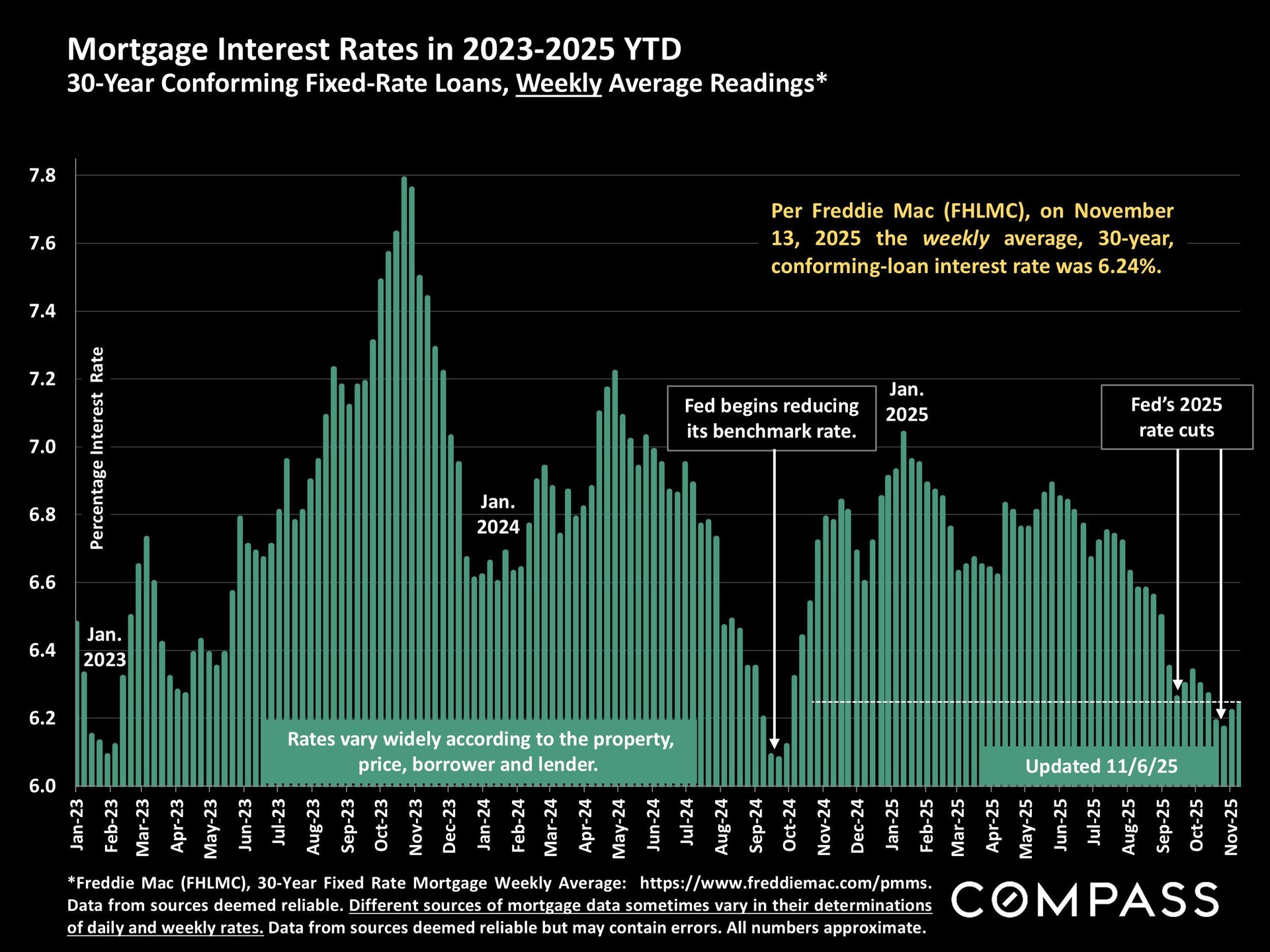

Rising Consumer Debt Stress

Debt strain continues to climb across multiple categories:

Credit Card Delinquencies

-

“Serious Delinquency” (90+ days) has more than doubled since interest rates began rising in 2022.

-

Delinquency rates are now at their highest percentage since 2012.

Higher interest rates + higher total credit card debt = increasing instability for many households.

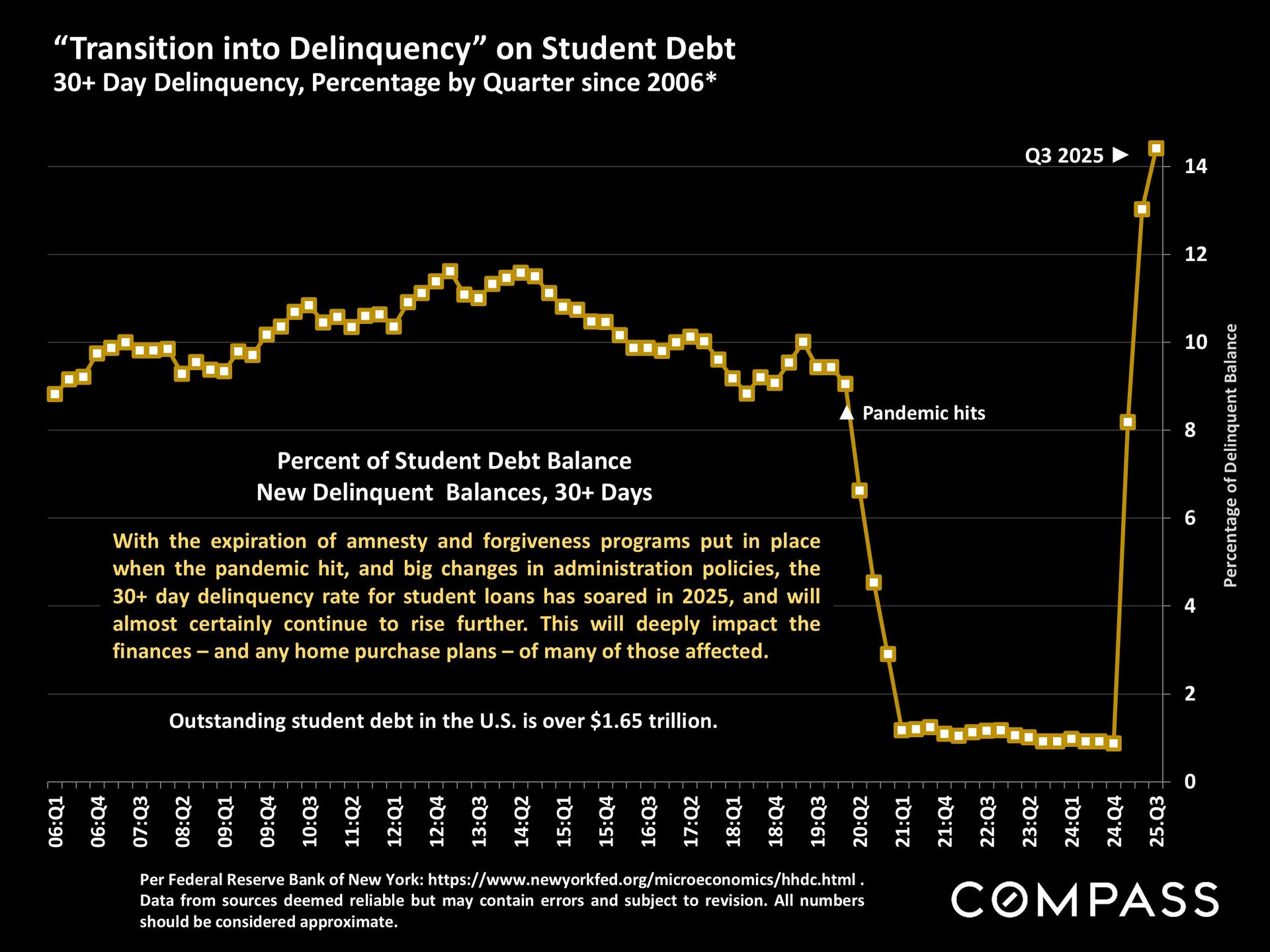

Student Debt

-

With pandemic-era relief over, 30-day delinquencies on student loans have begun climbing again.

-

Financial stress is growing especially for those who resumed payments in 2023–2024.

Auto Loans

From Bloomberg (11/12/25):

-

Subprime auto delinquencies (60+ days) hit 6.65% in October

-

This is the highest level in 31 years

Subprime borrowers rarely participate in Bay Area homebuying, but this illustrates broadening financial pressure.

Debt burdens are increasingly limiting potential first-time homebuyers, who face constrained affordability after years of rising prices and rising rates.

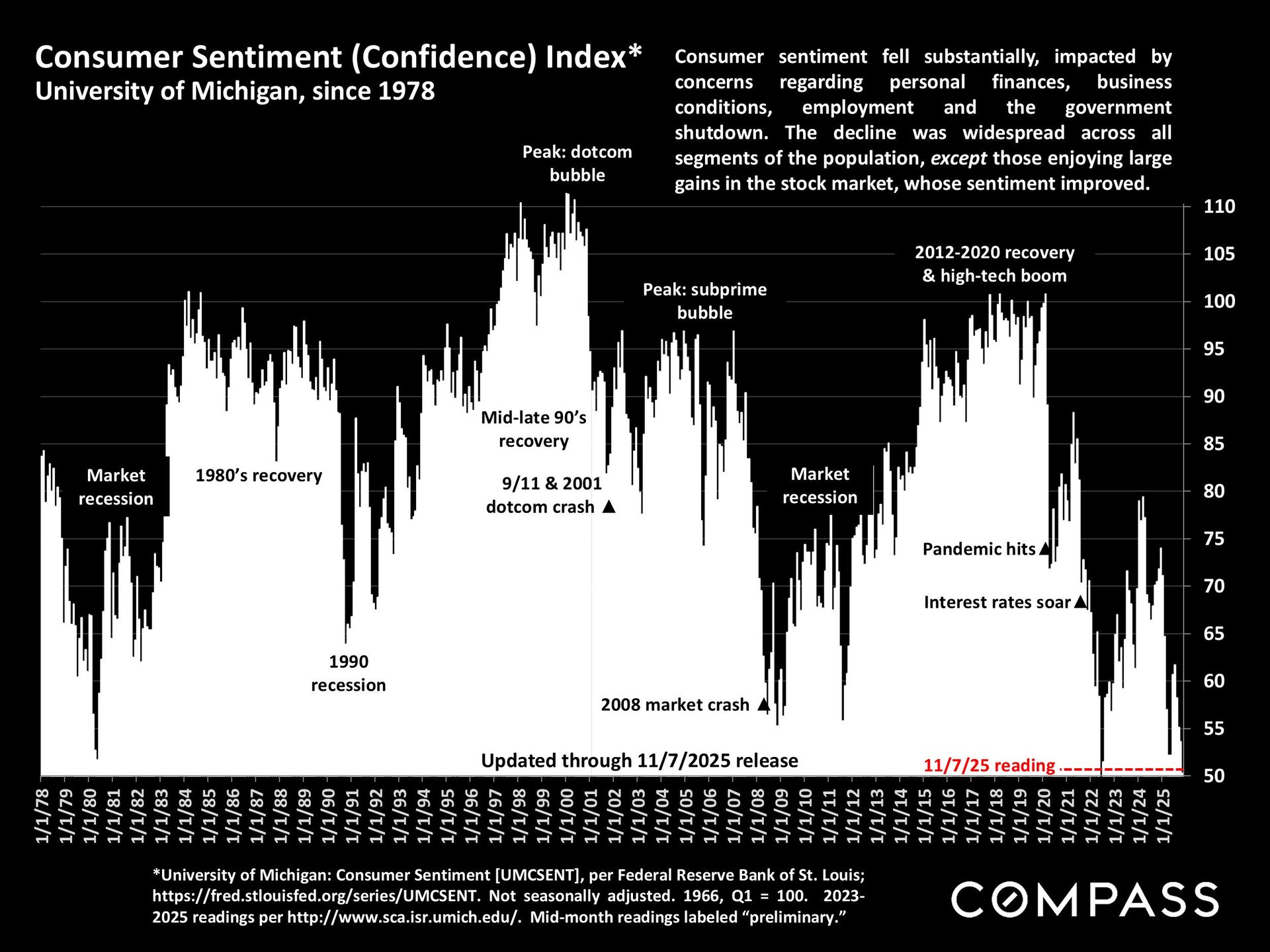

Financial Insecurity & Consumer Sentiment

Federal Reserve data and Consumer Sentiment indicators show:

-

Financial insecurity rose sharply in 2025 across most demographic groups.

-

The divide between affluent households (bolstered by stock market gains) and less affluent households is widening.

-

The Consumer Sentiment Index has fallen to near-historic lows.

-

Wealthier households-significant drivers of higher-priced market segments-are experiencing a very different economic reality than the broader population.

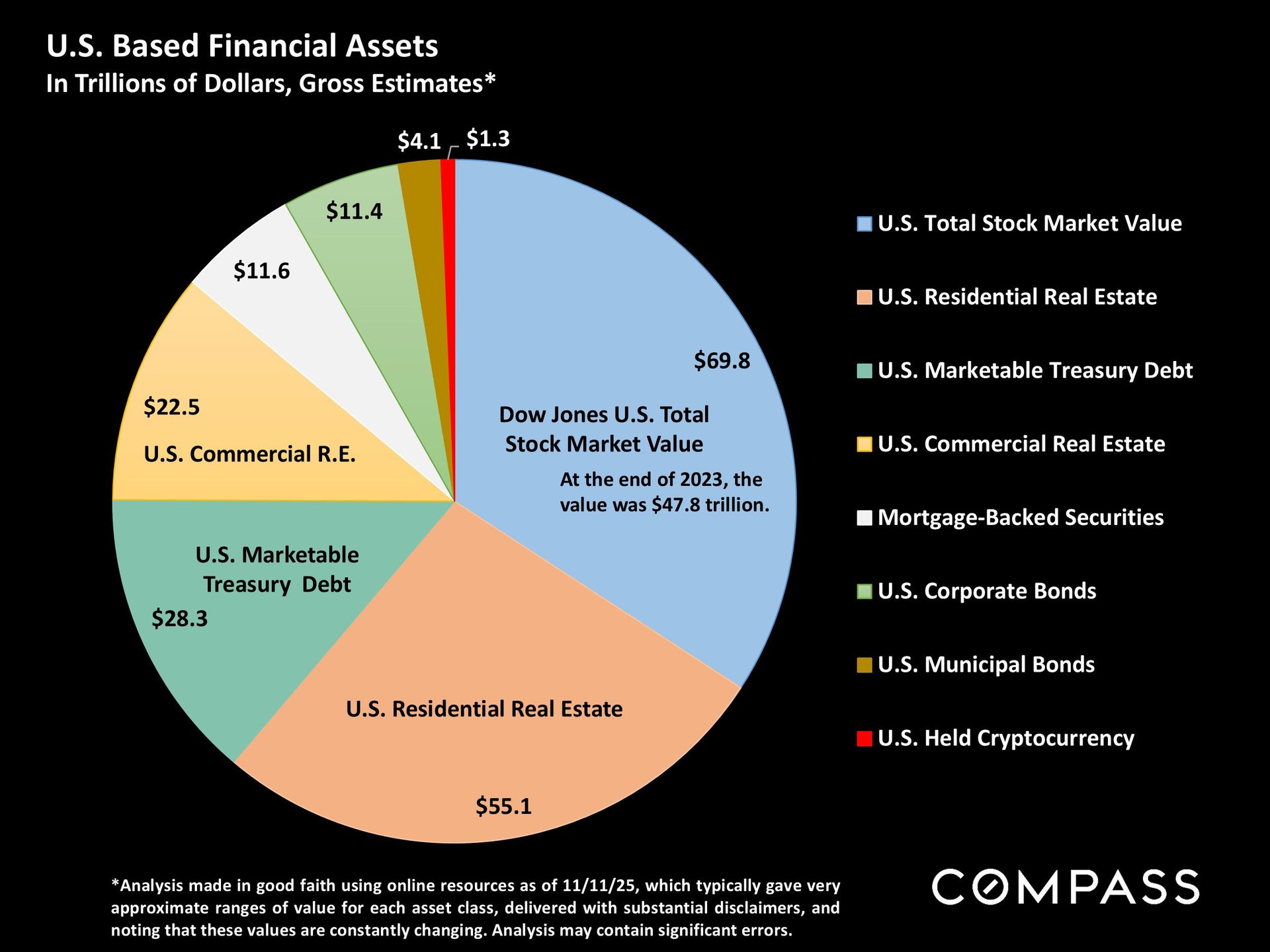

U.S. Financial Assets Overview

A Federal Reserve–based breakdown of U.S. financial assets shows the enormous scale of:

-

Stock market value

-

Residential real estate

-

Commercial real estate

-

Bonds, treasury debt, corporate debt

-

Mutual funds and ETFs

This context illustrates why changes in stock prices, bond yields, and real estate values ripple dramatically through both consumer psychology and housing demand.

Summary

Grounded fully in your uploaded data, here are the biggest takeaways:

-

The housing market is aging dramatically, hitting record-high median buyer ages.

-

Mortgage rates stabilized week-to-week but remain a key constraint.

-

Stock valuations are historically stretched, adding uncertainty.

-

Housing markets show regional divergence: Northeast/Midwest strength; South/Southeast weakness.

-

Condo markets are much softer than single-family markets nationally.

-

Bay Area sales dynamics are highly sensitive due to small inventory bases, especially in SF.

-

High-income job losses may alter demand patterns.

-

Consumer debt stress is rising across credit cards, student debt, and auto loans.

-

Consumer sentiment is near historic lows, with a widening gap between affluent and non-affluent households.

-

Broader financial assets remain concentrated in stocks and real estate, amplifying volatility impacts.