San Mateo County Real Estate Market Update - Through November & Early December 2025

The real estate market entered its typical mid-winter slowdown in November, with a significant drop in both new listings and sales activity. This seasonal contraction typically deepens through December-historically the slowest month of the year-before buyer activity and new inventory begin to re-emerge in mid-January.

Even as overall inventory shrinks, December often represents the best opportunity for motivated buyers to negotiate more aggressively, especially on properties with longer days-on-market. However, as is almost always the case, well-prepared and correctly priced listings can still attract immediate attention and sell quickly, sometimes above asking.

Looking Ahead to Early 2026

Attention now shifts toward early 2026. Historically, the start of the new year has ushered in a surge in buyer demand that then builds steadily into the spring market. This pattern briefly returned in early 2025 before being disrupted by the “tariff shock” and resulting economic uncertainty, which triggered a pronounced slowdown beginning in April.

This report reviews a selection of key market indicators through November and December 1st. The January report will reposition 2025 data into broader multi-year context.

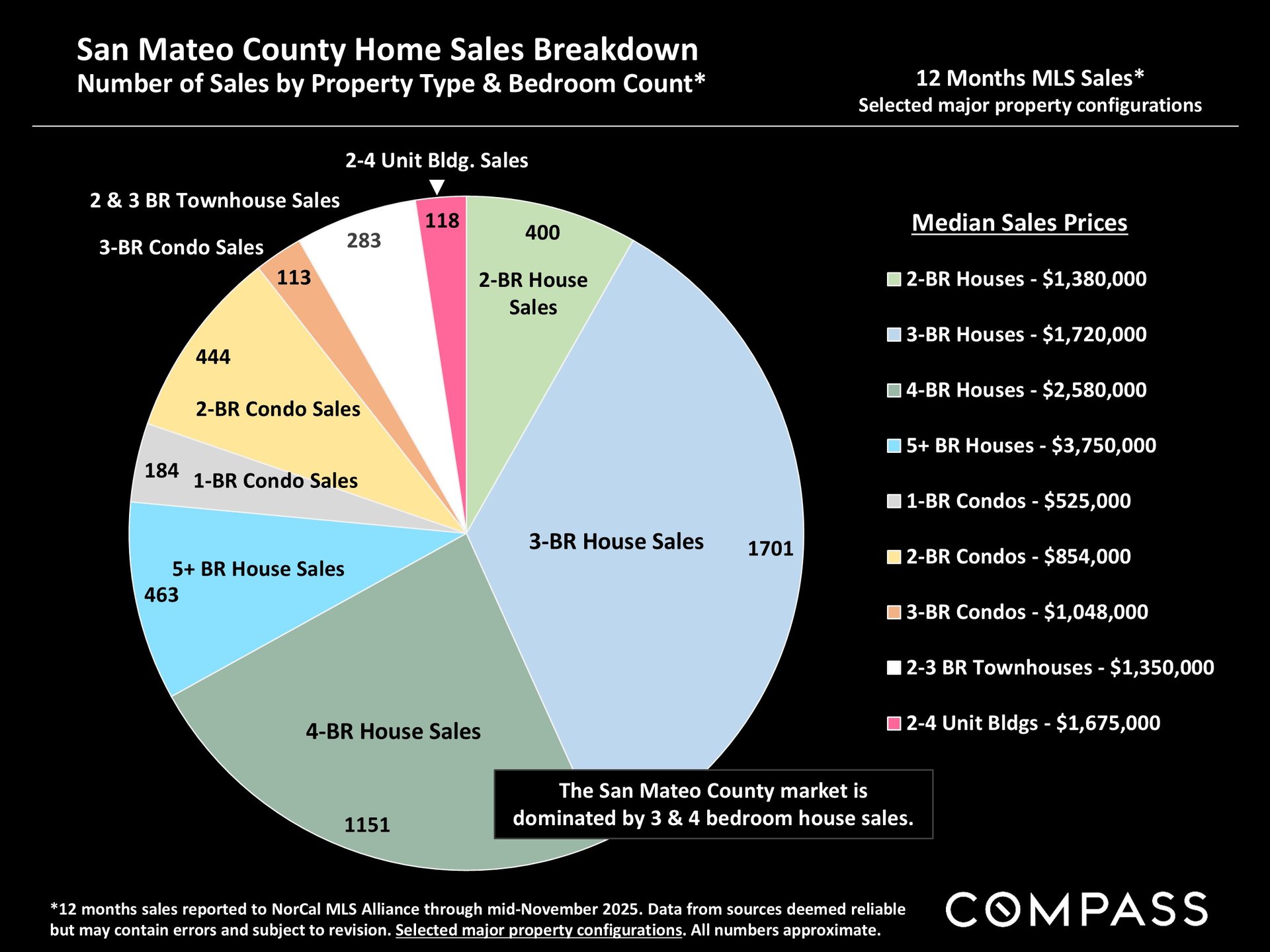

Home Sales Breakdown - Property Type & Bedroom Count

Sales over the past 12 months underscore the defining composition of the San Mateo County market:

-

3-bedroom houses dominate the market with 1,701 sales, representing the core housing stock.

-

4-bedroom homes followed with 1,151 sales, reflecting strong demand from move-up and larger households.

-

2-bedroom houses: 400 sales

-

5+ bedroom houses: 463 sales

Condo and townhouse activity is comparatively smaller:

-

1-bedroom condos: 184 sales

-

2-bedroom condos: 444 sales

-

3-bedroom condos: 113 sales

-

2–3 bedroom townhouses: 283 sales

-

2–4 unit buildings: 118 sales

Median Sales Prices illustrate the wide range of property types:

-

2-BR Houses: $1,380,000

-

3-BR Houses: $1,720,000

-

4-BR Houses: $2,580,000

-

5+ BR Houses: $3,750,000

-

1-BR Condos: $525,000

-

2-BR Condos: $854,000

-

3-BR Condos: $1,048,000

-

2–3 BR Townhomes: $1,350,000

-

2–4 Unit Buildings: $1,675,000

This configuration shows a market overwhelmingly driven by traditional single-family homes.

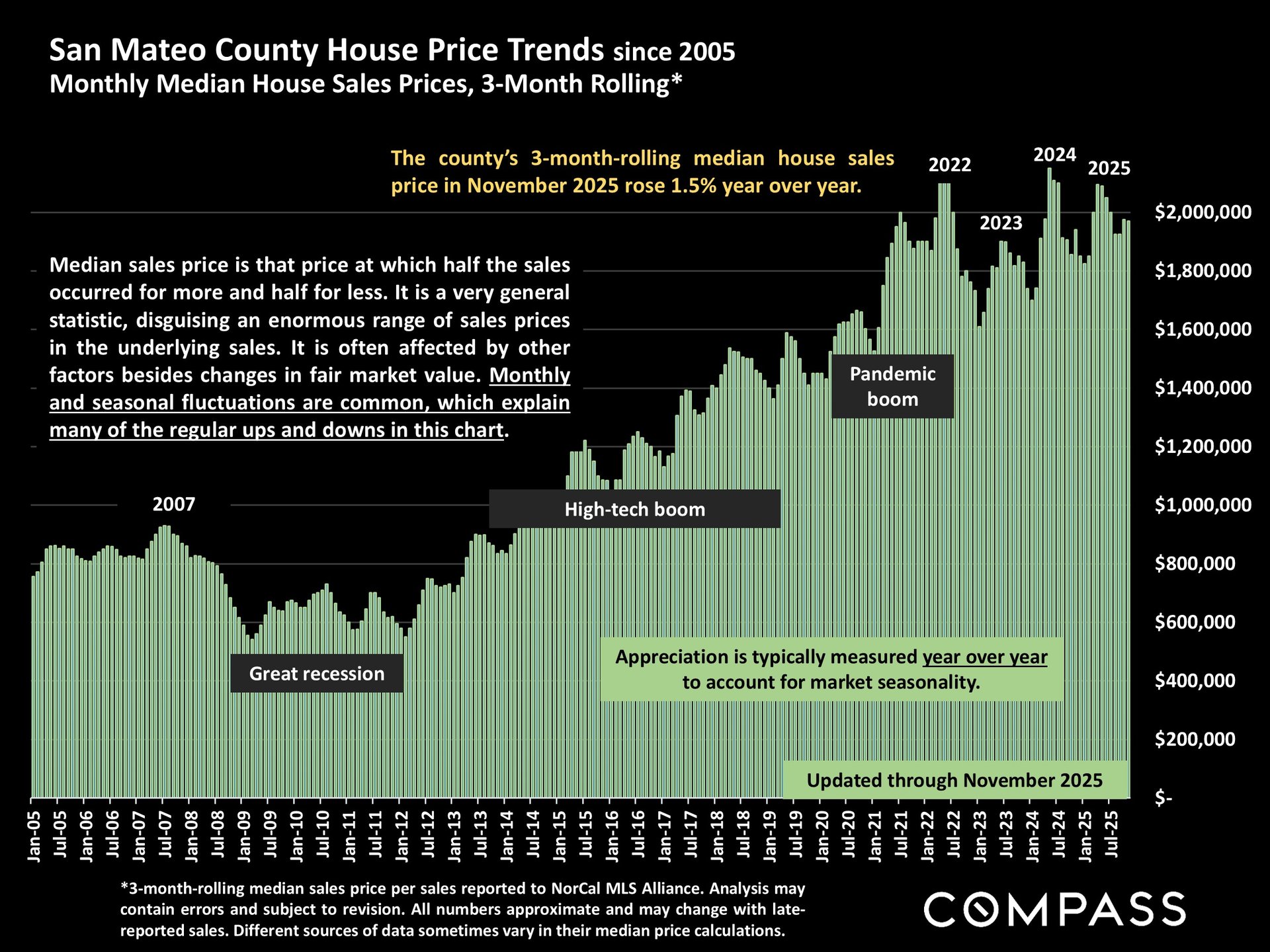

House Price Trends Since 2005

As of November 2025, the county’s 3-month rolling median house sales price rose 1.5% year over year, continuing a long-term upward trajectory despite mid-year turbulence.

Historical patterns remain clearly visible:

-

2007: market peak before the financial crisis

-

2008–2011: deep recessionary decline

-

2012–2018: strong recovery culminating in a high-tech boom

-

2020–2022: pandemic surge

-

2023–2025: a plateau with elevated prices, punctuated by volatility

Seasonality continues to drive notable ups and downs, but long-term appreciation remains strong.

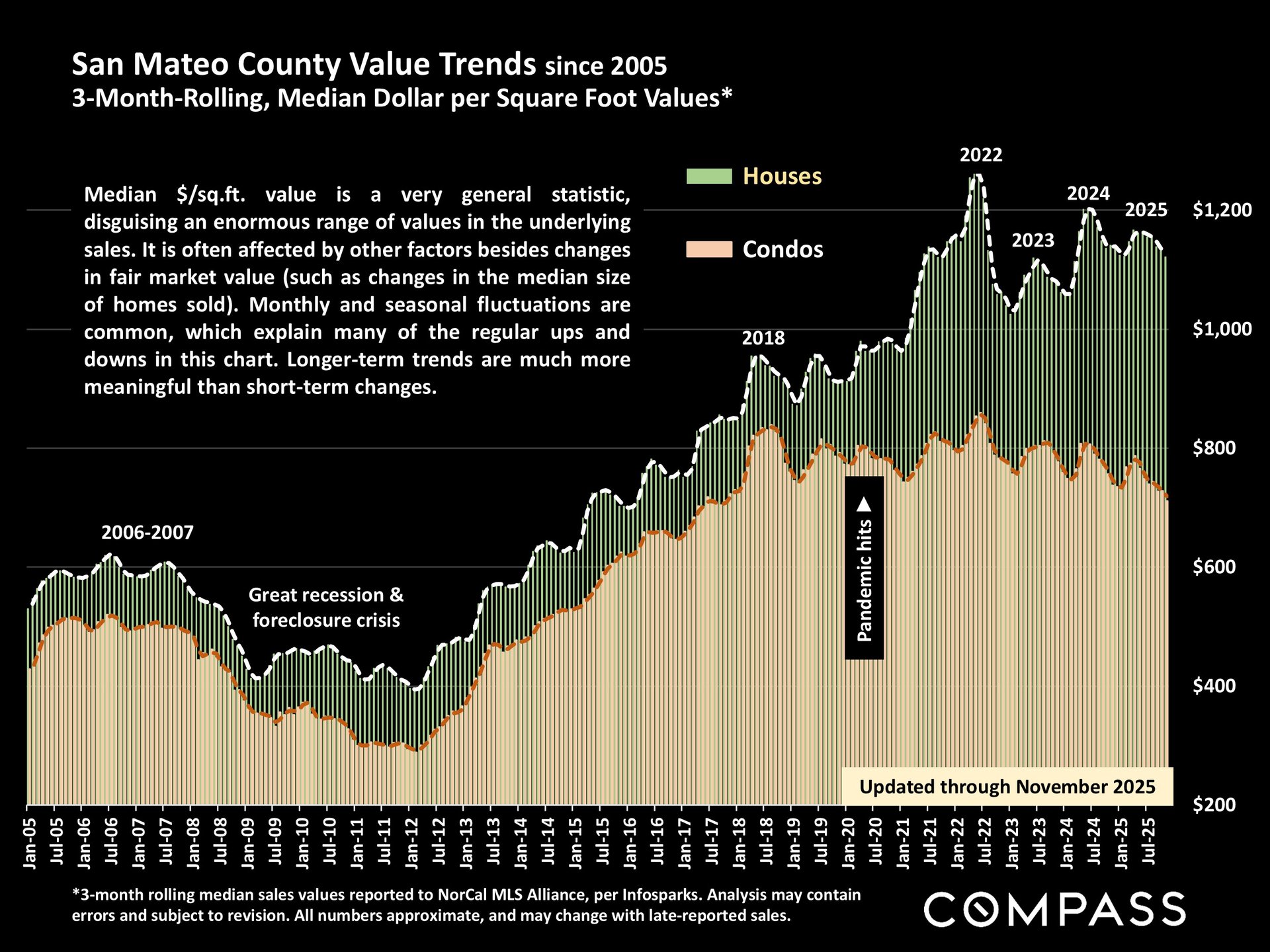

Value Trends – $/Sq.Ft. for Houses & Condos

The long-term $/sq.ft. trends emphasize the divergence between houses and condos:

Houses

-

Remain near historically high values first reached in 2022

-

Show stability year over year despite market headwinds

Condos

-

Continue a softer trajectory, with present values below their 2022 peaks

-

Show greater sensitivity to market fluctuations and buyer preferences

Both asset classes exhibit predictable seasonal movements, but houses maintain much stronger upward price resilience across cycles.

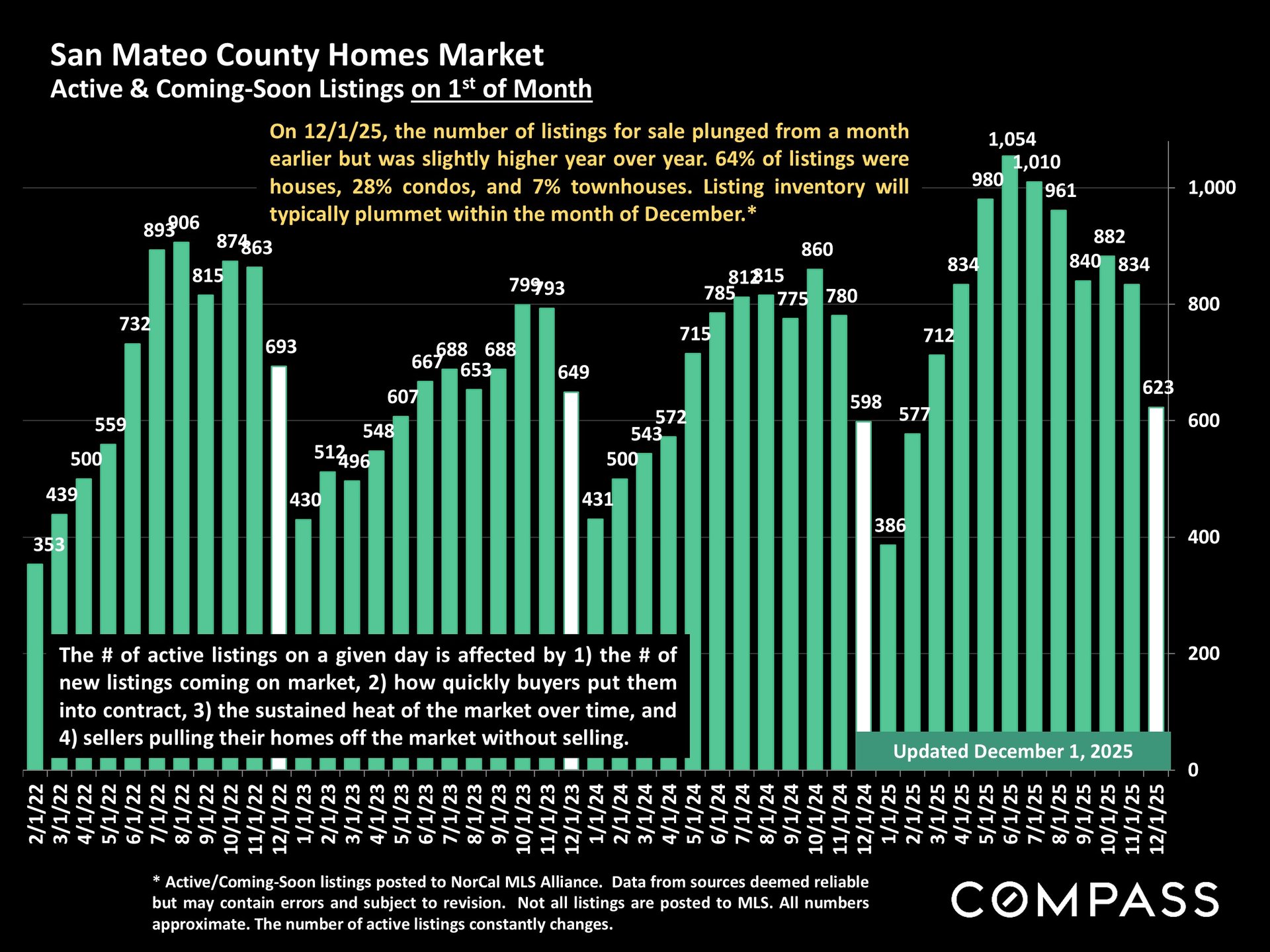

Active & Coming-Soon Inventory - As of December 1, 2025

Inventory levels experienced a steep month-over-month decline:

-

Listings dropped sharply from November, consistent with seasonal patterns.

-

Inventory is slightly higher year over year, suggesting a mild increase in seller participation.

Composition of current inventory:

-

64% houses

-

28% condos

-

7% townhomes

Historically, December is the month when listing inventory plummets, and this year appears aligned with that pattern.

Inventory levels are influenced by:

-

New listings brought to market

-

Buyers placing homes into contract

-

The sustained “heat” of any given market

-

Sellers withdrawing listings

Broader Financial Context

The first week of December saw the S&P 500 and Nasdaq recover much of their November decline, returning to near 14-month highs.

The 30-year mortgage rate remained close to its lowest point in over a year.

Consumer confidence ticked up modestly in November, but still sits at very low levels compared to long-term averages.

Markets now await:

-

A potential Federal Reserve benchmark-rate reduction

-

The upcoming inflation report later in December

Both events are expected to influence early-2026 housing dynamics.

Conclusion

San Mateo County’s late-2025 housing market reflects a classic winter slowdown layered over a year marked by unusual economic volatility. Inventory has contracted sharply, but well-priced properties continue to attract immediate interest. Single-family homes-particularly 3- and 4-bedroom configurations-remain the backbone of the market, displaying stable price appreciation even through mid-year disruptions.

Condo values continue to lag, and inventory patterns point toward a compressed December followed by a likely rebound in January. Broader financial markets add both tailwinds and uncertainty: mortgage rates are low relative to earlier 2025, equity markets are recovering, and economic sentiment remains fragile.

As the market approaches 2026, its trajectory will depend heavily on rate policy decisions, inflation data, and buyer confidence. Historically, early-year demand has reignited quickly, and if macroeconomic conditions stabilize, San Mateo County may see a renewed surge of activity moving into the spring.