Update on Economic Indicators

The economic landscape in early 2025 remains uncertain, shaped by fluctuating interest rates, declining consumer confidence, rising debt burdens, and volatile markets. Interest rates, which briefly climbed above 7% in mid-January, are gradually ticking downward, though mortgage rates remain elevated. Consumer sentiment has taken a sharp hit, and borrowing costs continue to strain households. Meanwhile, stock markets are grappling with a flood of complex economic and political variables, making future predictions challenging. As debt levels soar, concerns over long-term fiscal sustainability are growing.

Interest Rates and Borrowing Costs

Interest rates have started to ease after briefly exceeding 7% in mid-January. However, mortgage rates remain high despite the Federal Reserve cutting its benchmark rate. This is because mortgage rates are tied more closely to 10-year Treasury yields rather than short-term Fed rates.

The bond market has been digesting a mix of economic data, inflation trends, and political developments. Since the Fed’s September rate cut, the 10-year Treasury note yield has risen, keeping mortgage rates higher than expected. Additionally, as federal debt continues to flood the market, investors are demanding higher interest rates on Treasury notes, making long-term borrowing more expensive. Many economists warn that federal debt levels are growing at an unsustainable pace, contributing to prolonged high mortgage rates.

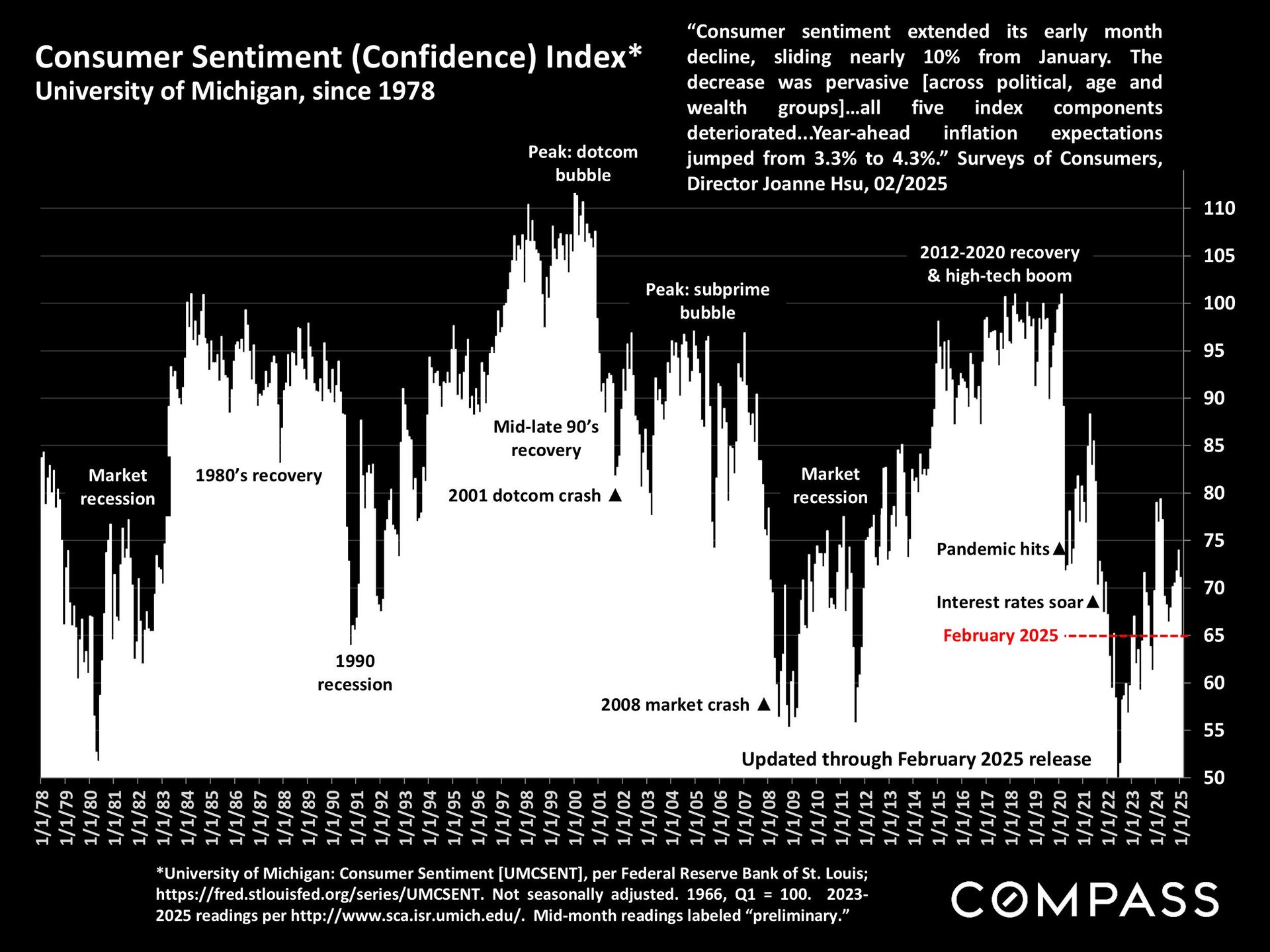

Consumer Confidence and Spending Behavior

Consumer sentiment has declined sharply across all demographics, reflecting growing unease about inflation, employment, and economic stability. According to the University of Michigan Surveys of Consumers, confidence dropped across all five index components, with the steepest declines among those aged 35 to 55.

A separate measure, The Conference Board Consumer Confidence Index®, recorded its largest monthly drop since August 2021. This marks the third consecutive decline, bringing the index to its lowest level since 2022. While consumers’ views of current business conditions improved slightly, expectations for future employment, income, and economic stability worsened significantly. This decline in sentiment is expected to weigh on consumer spending, particularly for big-ticket purchases that require financing.

Debt Pressures and Loan Delinquencies

Rising interest rates on credit cards are putting significant financial strain on consumers. Over the last decade, the average APR on credit cards has nearly doubled, reaching a record-high 24.2% in February 2025. As a result, credit card delinquencies—defined as accounts overdue by 90 days or more—have climbed to their highest level since 2012.

Auto loan delinquencies are also on the rise, exacerbated by higher interest rates on car loans. Many consumers who financed vehicles at historically low rates in previous years are now facing much steeper borrowing costs, leading to increased payment struggles.

Despite these challenges, mortgage delinquencies remain historically low. Many homeowners locked in fixed-rate loans before 2022, shielding them from rising borrowing costs. Additionally, continued home price appreciation has prevented widespread mortgage distress, as homeowners maintain equity in their properties.

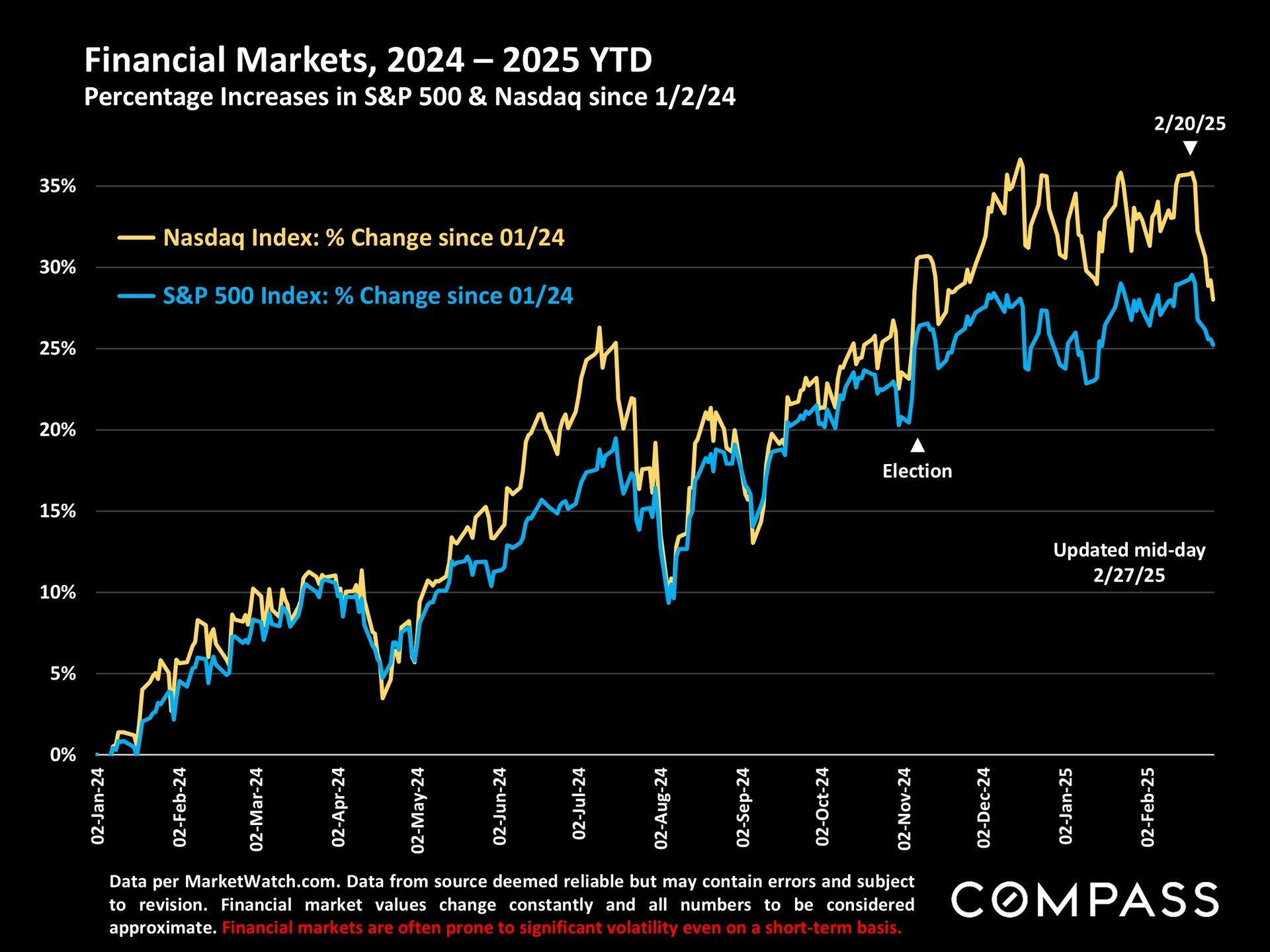

Stock Market Volatility and Margin Debt Surge

Stock markets have had a rough week as investors try to interpret a vast number of uncertain political and economic variables. However, given the extreme volatility seen over the past 14 months, drawing firm conclusions about future trends remains difficult.

One concerning trend is the sharp rise in securities margin debt between January 2024 and January 2025. Margin debt, which involves borrowing money to invest in stocks, has surged, suggesting a wave of investor optimism—or potential overconfidence. While margin debt can fuel market gains, it also increases the risk of sharp downturns if stock prices fall and investors are forced to sell assets to cover debts.

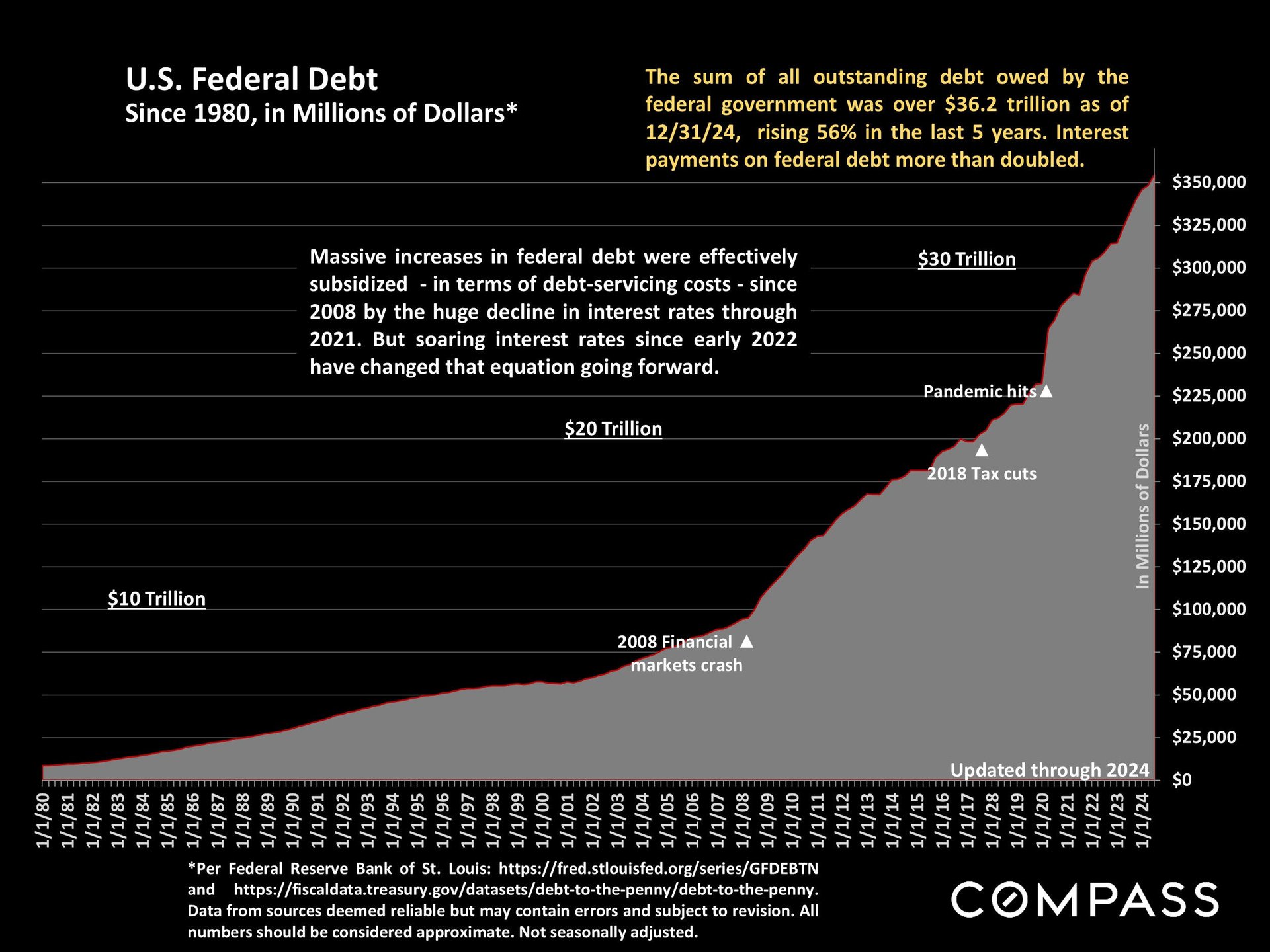

Federal Debt and Economic Stability

The rapid expansion of federal debt remains a major concern for economists. As interest rates have risen over the past few years, the cost of servicing this debt has skyrocketed. The increase in federal debt interest payments is adding pressure to government budgets and raising questions about long-term fiscal sustainability.

At the heart of this issue are tax policies and federal spending, both of which are currently in political flux. Tax receipts from individuals and corporations fluctuate based on legislative changes, while government expenditures remain a hotly debated topic. If federal borrowing continues at its current pace, investors will likely demand even higher interest rates on Treasury bonds, which could keep borrowing costs elevated for years to come.

Conclusion and Future Outlook

The U.S. economy is navigating a delicate balance between inflation, interest rates, consumer confidence, and fiscal stability. While interest rates are edging downward, mortgage rates remain high due to Treasury market dynamics. Consumer confidence has taken a significant hit, particularly regarding future employment and income expectations. Debt burdens are mounting, with credit card and auto loan delinquencies reaching decade highs, though mortgage delinquencies remain low. Meanwhile, the stock market remains volatile, with rising margin debt pointing to heightened speculation.

As federal debt continues to grow, the long-term outlook for interest rates and borrowing costs remains uncertain. The coming months will be crucial in determining whether inflation slows, confidence rebounds, and economic conditions stabilize. Policymakers, businesses, and consumers alike will need to stay vigilant as they navigate an increasingly complex economic landscape.